(Zero Hedge)—More than 50% of parents with a child older than 18 are providing them with at least some financial support, according to a recent report by savings.com.

Key findings from the report:

- Half of parents with adult children provide regular financial assistance to their grown offspring. The average support per adult child is $1,474 monthly, about 6% higher than last year.

- 83% of supporting parents contribute to their adult kids’ monthly groceries; 65% help with cell phones, and nearly half (46%) pay for vacations.

- More than three-quarters (77%) of supportive parents attach conditions to their financial assistance. 23% give money without any conditions.

- Nearly 50 percent of parents have sacrificed their financial security to help their grown kids financially, and most supporting parents feel obligated to help their kids with money.

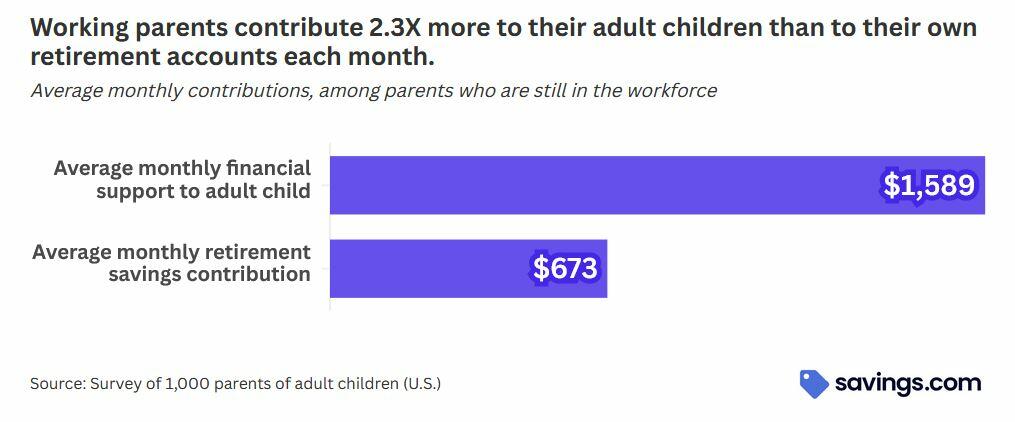

- Working parents who support grown kids contribute over 2X more money each month to their adult children than they do to retirement funds.

As savings.com continues, with inflation keeping the cost of living high, parents’ financial support has reached a new peak, averaging nearly $1,500 per month (or almost $18,000 annually). This represents a six percent increase from the monthly contributions we reported last year.

As you might expect, Generation Z adults (ages 18-28) receive more financial support from their parents than their Millennial counterparts (ages 29-44), who’ve had more time to build careers and establish income streams. While the average contribution to Millennials decreased slightly, a significant increase in support for Generation Zers pushed the overall average higher. Members of Generation X (ages 45-60) rarely receive financial assistance from their parents, likely because they’ve either achieved financial independence or have inherited family wealth.

The financial strain of supporting grown children is particularly pressing for parents preparing a nest egg. Parents still in the workforce contribute over two times more money to their adult children each month than their retirement accounts.

The psychological and fiscal impact of such commitment translates directly to parental anxiety. At a time when many Americans haven’t set aside enough funds for their later years, 79 percent of those supporting adult children worry about setting themselves up for a comfortable retirement. In comparison, 72 percent of people who don’t support adult children financially feel stressed about their retirement savings.

What costs do parents cover for their adult children?

Parents report providing their adult children with financial assistance for various expenses, from educational costs to vacations to basic spending money.

Looking at the breakdown of this support reveals that food and groceries top the list of needs among financially dependent adult children. With food prices continuing to climb, it’s understandable that four out of five parents providing assistance are helping with their grown kids’ grocery bills. Parents contribute an average of $220 monthly toward their adult child’s grocery expenses.

Another two-thirds of parents with adult children assisted with cell phone bills and housing expenses. The need for specific types of support varied between Generation Zers and Millennials. Gen Z adults were far more likely to need help with healthcare, vacations, and tuition than Millennials, as many are still in school or just launching their careers in their early twenties. School expenses were the costliest for parents, averaging nearly $1200 monthly. That’s a massive increase over the average spending on tuition last year, at around $600 a month.

Parental financial support often comes with conditions

Accepting financial help from parents is one thing, but doing so while demonstrating effort and appreciation is another matter. Our findings suggest that parents may be growing less tolerant of adult children who appear to take advantage of their generosity.

Among parents providing financial support, 63 percent also offer housing to their adult children. While only 39 percent of these live-at-home adult children contributed to household expenses in 2024, that figure has increased substantially to 51 percent this year.

This improvement in shared financial responsibility likely stems from parents setting firmer boundaries. The percentage of parents establishing specific conditions for financial assistance has increased since our previous study—from 71 percent who gave conditionally last year to 77 percent who now attach requirements to their financial support.

The most notable increase appeared in parents requiring adult children living at home to contribute to household expenses. However, the most common conditions continue to be requirements that adult children actively seek employment or pursue education—practical approaches designed to guide grown offspring toward eventual financial independence.

Other conditions parents placed on their adult children included establishing financial goals and attending counseling or therapy sessions. Each such requirement reflects a caring concern designed to help adult children financially get on their feet.

What are parents sacrificing for their children’s financial security?

The parents in the study seemed more than willing to aid their children. Yet, that added financial burden often creates stress and demands lifestyle sacrifices. What compels them to keep giving?

Obligation is one driving force for parents who economically support their adult offspring. Most parents who provide monetary assistance do so out of some sense of duty.

Fifty-three percent of contributing parents feel responsible for financially supporting their grown kids. That number is down from 61 percent one year ago, another potential indicator that such gravy train sentiments may be slipping.

This responsibility causes great strain on parents. Nearly 50 percent of providing parents sacrifice financial security for the sake of supported children, and 40 percent felt pressured to give financial assistance even when it meant uncomfortably stretching their resources.

Those numbers mirror the findings from past reports. Despite the hardship and stress sometimes created by these contributions, devoted moms and dads remain ready to dig deeper to help their struggling kids. Nearly nine in ten parents would make one or more additional financial sacrifices to aid their offspring.

Specifically, more than 60 percent of parents would be willing to live a more frugal lifestyle to support their adult children, half would pull money from their savings or retirement accounts, and one-third would postpone retirement or take on debt so that they might shift funds to provide for their progeny.

Many supporting parents would be willing to come out of retirement or refinance their homes to help their children. Grown kids struggling through financial straits are fortunate to find such selfless family support. They shouldn’t take it for granted or become perpetually dependent.

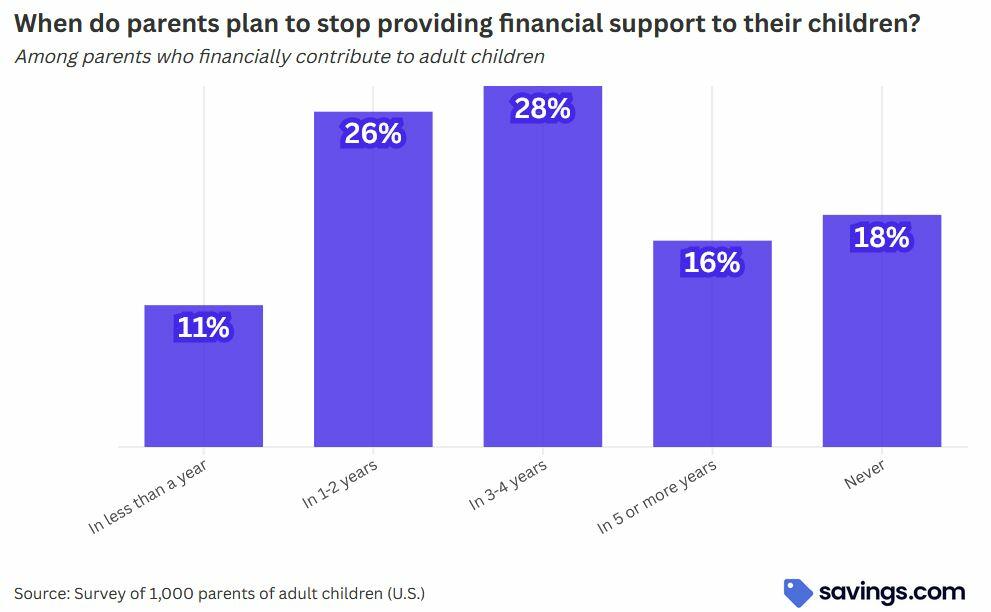

When asked how long they planned to continue financial support of adult children, parents admitted there may be a shelf life on their generosity. Less than 20 percent of those supplying aid said their largesse would continue indefinitely.

More than one-third of parents who give money to their adult kids say they’ll cut off support within the next two years. Their aim is likely to encourage their children towards financial independence. However, terminating assistance before a potential recession could deal a double blow to younger generations.

Conclusion

The last four years of our research findings collectively illustrate remarkable parental commitment. Parents continue to accept financial stress and make personal sacrifices to support their adult children’s economic well-being. However, even as we see more parents providing financial assistance than in any previous year of our research, we’ve also detected some emerging cracks in this foundation of support.

The percentage of parents who feel financially responsible for supporting their adult children has declined, while more are establishing specific conditions for continued assistance. Perhaps most notably, almost 40 percent of parents plan to end their financial support within the next two years.

Despite these subtle shifts away from unconditional assistance, our survey essentially confirms what we’ve seen in recent years: the ongoing need to financially support struggling adult children is placing significant strain on many parents’ financial security. This concerning pattern may face additional pressure if economic conditions worsen in the coming months. We’ll examine how these trends evolve in our 2026 report.

Bypass Big Tech Censors

Safeguarding Your American Dream: Discover the Power of America First Healthcare

In today’s economy, healthcare costs remain one of the biggest threats to financial stability and family security. Americans work hard to build a better life, yet rising medical expenses can quickly erode savings, force tough trade-offs, and even push families toward debt or bankruptcy. Medical bills continue to rank as the leading cause of personal bankruptcy in the United States, with millions facing underinsurance or unexpected out-of-pocket burdens that no one plans for. Many turn to government-run marketplace plans under the Affordable Care Act, hoping for relief, only to discover that what appears affordable on paper often delivers higher long-term costs, limited real protection, and coverage that may not align with personal values or family needs.

America First Healthcare stands out as a private insurance agency dedicated to helping conservatives and families secure better coverage and better rates through customized, values-aligned options. By conducting free insurance reviews, the agency uncovers hidden gaps in existing policies and connects clients with private alternatives that emphasize personal responsibility, small-government principles, and genuine affordability—often delivering up to 20% savings while providing stronger protection for the American Dream.

The allure of marketplace plans is easy to understand: open enrollment periods, premium tax credits for many households, and the promise of “comprehensive” benefits mandated by law. Yet recent data reveals a different reality, especially after the expiration of enhanced premium subsidies at the end of 2025. Enrollment for 2026 dropped by more than one million people compared to the prior year, with many shifting to lower-tier bronze plans to keep monthly premiums manageable.

These plans feature significantly higher deductibles—averaging around $7,500 nationally—and greater cost-sharing requirements. Families who once paid modest amounts after subsidies now face average premium increases of $65 or more per month, even as they accept plans that leave them responsible for thousands in upfront costs before meaningful coverage kicks in.

High deductibles create a dangerous barrier to care. Studies show that people in such plans are less likely to seek timely treatment for chronic conditions, attend preventive screenings, or fill necessary prescriptions. A seemingly minor illness or injury can balloon into major expenses when patients delay care until problems worsen. For a family of four, a single hospitalization, cancer diagnosis, or unexpected surgery can easily exceed the deductible, triggering coinsurance and out-of-pocket maximums that still leave substantial bills. One recent analysis noted that some proposed changes could push family deductibles toward $31,000 in future years, further exposing households to financial risk.

Beyond the numbers, marketplace plans often carry structural limitations. Coverage for certain critical services may include waiting periods or narrower networks that restrict access to preferred doctors and specialists. Preventive care is required to be covered without cost-sharing, but everything else—lab work, imaging, specialist visits, or ongoing treatment—typically waits until the deductible is met. This reactive model contrasts sharply with the proactive, holistic approach many families prefer, especially those focused on wellness, early intervention, and maintaining health to enjoy life rather than merely reacting to illness.

Values alignment represents another growing concern. Government-influenced plans operate within a framework shaped by federal mandates and political priorities that may not reflect conservative principles of limited government, personal freedom, and ethical stewardship. Families who want to direct their healthcare dollars toward providers and benefits that honor traditional values sometimes find marketplace options feel misaligned, forcing a compromise between affordability and conviction.

Private alternatives, by contrast, offer year-round flexibility without the restrictions of open enrollment windows. Independent agents can shop across a wider range of carriers to design plans tailored to specific family needs—whether that means lower deductibles for frequent medical users, broader provider networks, or add-ons that support wellness and preventive services from day one. Clients frequently report more stable premiums that do not automatically escalate each year, along with genuine cost savings once the full picture of deductibles, copays, and coverage depth is considered.

Take the experience of real families who made the switch. Amanda C. shared that her new plan felt “way better” than what she had through the marketplace. Johnny Y. noted his previous coverage kept increasing annually until he found a more stable private option. Sofia S. expressed delight with her plan and began recommending it to others. These stories echo a common theme: when families move beyond one-size-fits-all government marketplaces, they often discover customized protection that better safeguards both health and finances.

Founder Jordan Sarmiento’s own journey underscores the stakes. In 2021, a six-day hospitalization generated a $95,000 bill. Under a well-structured private “Conservative Care Coverage” plan, his out-of-pocket responsibility would have been just $500. That stark difference illustrates how thoughtful planning and private options can prevent a medical event from becoming a financial catastrophe.

Practical steps exist for anyone questioning their current coverage. Start with a no-obligation review of your existing policy to identify gaps—high deductibles, limited critical-care benefits, or escalating premiums. Compare total projected costs (premiums plus potential out-of-pocket expenses) rather than monthly premiums alone. Consider family health history, anticipated needs, and lifestyle priorities. Private agencies can present side-by-side options that include stronger wellness incentives, broader access, and plans built on shared values of self-reliance and freedom.

In an era when healthcare inflation continues to outpace general cost-of-living increases, relying solely on marketplace solutions carries growing risk. Families who proactively explore private alternatives frequently achieve meaningful savings while gaining peace of mind that their coverage truly works when needed most.

America First Healthcare makes this exploration straightforward through its free review process. Families and individuals receive personalized guidance to close coverage holes, reduce unnecessary expenses, and secure plans that align with conservative principles—protecting wallets, health, and the American Dream without government overreach. Many who complete a review discover they can enjoy better benefits for less, often saving up to 20% while gaining the customization and stability that marketplace plans struggle to deliver.

Ultimately, protecting your family’s future requires looking beyond the marketing of “affordable” government options. By understanding the long-term costs hidden in high deductibles, shifting coverage tiers, and values mismatches, Americans can make empowered choices. Private, values-driven insurance offers a smarter path—one that rewards diligence, supports wellness, and delivers real security. For those ready to move beyond the limitations of traditional marketplace plans, a simple review can reveal options designed to serve families, not bureaucracies. The American Dream thrives when individuals and families retain control over their healthcare decisions, and thoughtful private coverage plays a vital role in making that possible.